Table of Content

- What's the Difference between a Home Construction Loan and a Mortgage?

- Home Loans and Mortgages | New Prague, MN

- Home Financing Options

- LOAN REQUIREMENTS

- Get Connected With The Right Lender For You

- Construction Loans: Everything You Need To Know

- Subscribe to our newsletter and receive expert advice on buying, building, and owning your home!

If you’d act as your own general contractor, meaning you’d DIY the entire project, you’d be less likely to get approved, so take note of that. But you have one more option, which is an owner-builder construction loan. You just have to prove your ability and knowledge in construction, otherwise, lenders may deny you funds. If you don’t want to build a home from the ground up, but only restore an old property, a construction loan might work for you as well.

If the borrower fails to make their mortgage payments, the lender can foreclose on the home and collect the proceeds from the sale to pay off the loan. If you’re unsure how to assess your ability to repay, get pre-approved for a mortgage. If your pre-approved loan amount is smaller than the value of the house you want, you can wait it out and grow your income first. Once you become more financially capable, you can afford to build instead, and enjoy a custom-built abode. But in terms of convenience, affordability, and conditions, the two aren’t the same.

What's the Difference between a Home Construction Loan and a Mortgage?

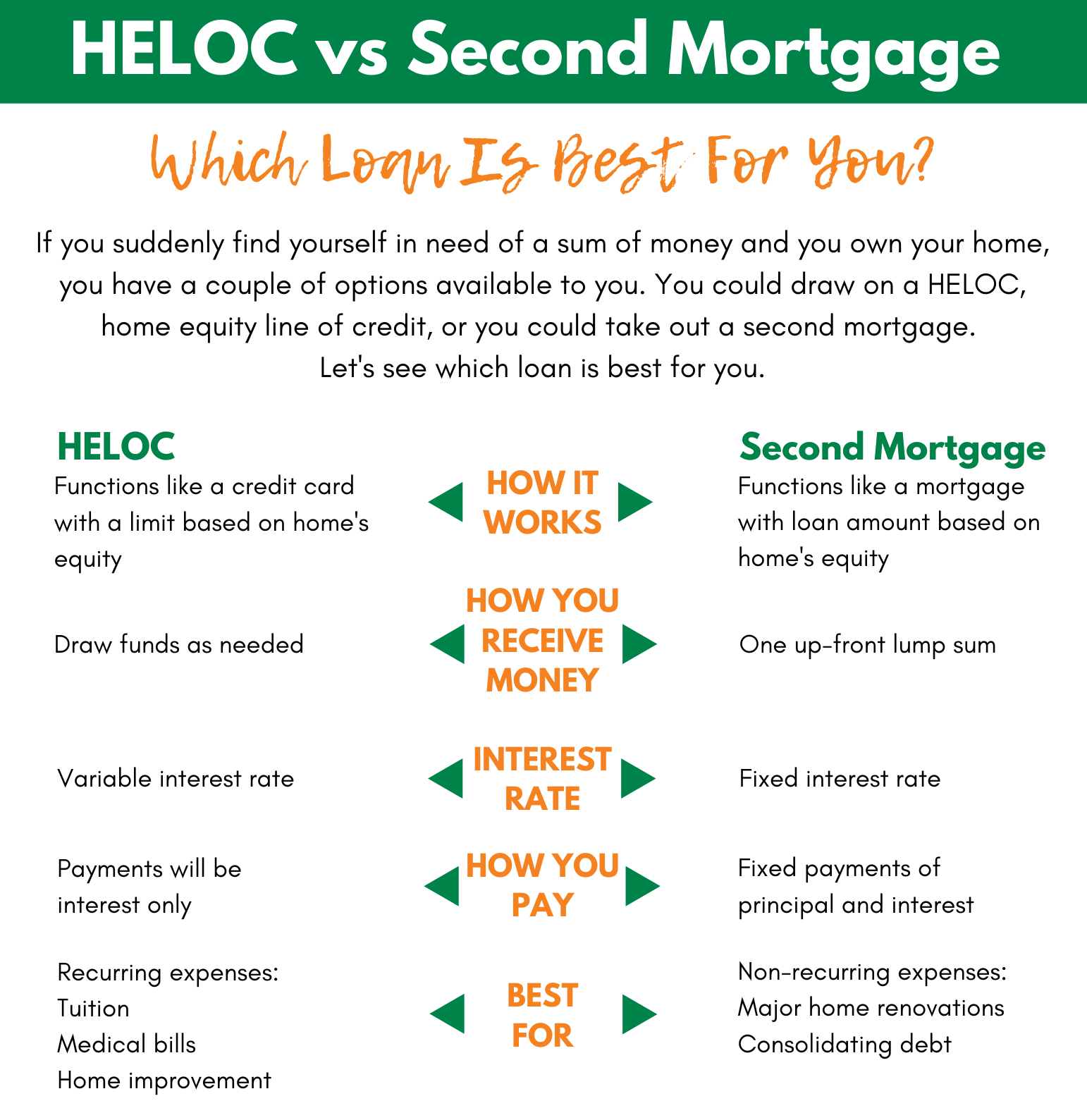

But it’s the only way to end up with a place customized exactly according to your desires. Home loans and construction loans are different, but at Granite Companies, we can help you find the right loan for the project. The easiest way to make the decision is to determine whether you have enough home equity to qualify for the appropriate size of HELOC that you need for your project. If you don’t have that equity yet, a construction loan of some kind is going to be your best bet. Construction loans are another avenue for anyone who wants to build new construction or undertake a major home renovation but doesn’t have home equity yet. The idea behind these loans is that the future home or modified home will create the secured value for the costs incurred.

Banks and financial institutions offer different types of home loans. Depending on the purpose behind the need for capital, the type of loan is determined. For instance, if you would like to purchase a home, a home loan would be recommended. We will also understand the difference between them with a home loan comparison.

Home Loans and Mortgages | New Prague, MN

Once the term ends, you’ll then have to repay the total amount or convert it into a mortgage. Remember that making interest-only payments means you aren’t building equity — even though you’re making payments on your home. Construction Loans typically require a larger down payment than traditional mortgage loans, and the interest rates tend to be higher as well.

Apply online for expert recommendations with real interest rates and payments. With so many factors to consider while house hunting – including house style, size and location, just to name a few – sometimes people don’t know where to even start. This is why people believe they either need loads of cash, or, the ability to obtain a construction loan, if they want to buy a home. This existing home is used as collateral should the borrower default on their loan. However, when building a home, there is no collateral since there is no existing home to secure the loan.

Home Financing Options

Though it’s generally cheaper to buy a home than to build one, it doesn’t automatically mean a mortgage gives you an edge. If the interest rates are at an all-time high, that would increase your monthly payments. On the other hand, if you got a fixed-rate mortgage and the interest rates drop, you’d still be paying the constant interest of your loan, even if it’s higher. Construction loans often have higher interest rates because they’re riskier than a mortgage. Their terms only last for about a year, which is the usual period a home takes to finish building.

Often, the construction loan balance gets rolled into the new mortgage loan. Usually, a builder or contractor takes out the construction loan and pays back the loan. Many institutions prefer to lend to both the contractor and the buyer as the end-financer. Any remaining costs of construction can be paid down by acquiring a mortgage on the home once it’s completed. Your mortgage terms will vary from lender to lender, but will generally last for 10 to 30 years, depending on your interest rate and monthly payments. Qualifying for a construction loan may require a larger down payment and more paperwork than a typical mortgage.

LOAN REQUIREMENTS

Expect to have between four and six inspections to monitor the progress. The key advantages of this unified approach are that you only have to pay one set of closing costs, and you don’t have to go through two separate application processes. While both loans are types of mortgage loans, there are many significant differences between a Home Loan and a Construction Loan.

This allows borrowers to both purchase and renovate their new home while still making one monthly payment to cover both costs. Conventional loan borrowers may qualify for these loans through Fannie Mae and Freddie Mac . This type of loan is short-term and is usually issued for a year. With so many variables like the builder’s cooperation, getting approvals from local municipalities and more, these are considered higher-risk loans.

In the mornings I would throw on my jogging gear and enjoy a nice stroll around the park's trails, trees, and ponds. On my jog back to the house, I would pass the University of New Hampshire's Franklin Pierce School of Law, a beautiful brick institution. My environment, with its natural beauty, a wealth of education, and historical architecture, provided me with enthusiasm and enlightenment every morning. Watching the hustle and bustle of this scene is like observing the actors on a film set rushing off to be in position for their parts. As I finish up coffee, I am occasionally delighted by the presence of a friendly face or two, I beckon them over, and we initiate our day with coffee and comradery. The day does start eventually, even in this quintessential New England city, and I rush off to work.

The initial loan term generally lasts the length of your construction project. If you can’t find the right home to buy, you might be thinking about how much it will cost to build a new house or renovate the one you currently call home. The process of borrowing the money to pay for this project is different from getting a mortgage to move into an existing property.

Cost of building a home, including the land, labor, materials and permits. The approval process for a construction loan is similar to that of a typical mortgage in that you’ll need to apply and submit documentation to your lender. In home loans, a borrower takes money from a bank to either buy a house or flat or to build a new house. You can take a home loan to renovate your existing house or for buying land as well. This type of loan is usually a secured form of loan wherein the house for which the loan is being taken is held as collateral by the lender. It is released when the entire loan is repaid in the form of monthly instalments by the borrower.

If you’re like many people, you might not have the cash on hand to pay the entire cost upfront. This is because mortgages requires some sort of asset or collateral to back the loan. To explain further - a mortgage is used to finance the purchase of an existing home. A construction loan is used to finance the construction of homes, vacation homes, commercial buildings, offices, etc. When it comes to building a house, most people assume that you need to have deep pockets to obtain a construction loan. If you have good credit and a strong financial history, a home construction loan may be a good option.

If you're planning to build a home in Canada, you'll likely need to take out a loan to finance your construction. But between a construction loan and a mortgage, which one should you get? Both have their own advantages and disadvantages, so it's important to understand the difference between the two before you decide which one is right for you.

No comments:

Post a Comment